India's 2026 FDI Update: The New 10% "Beneficial Ownership" Rule Explained

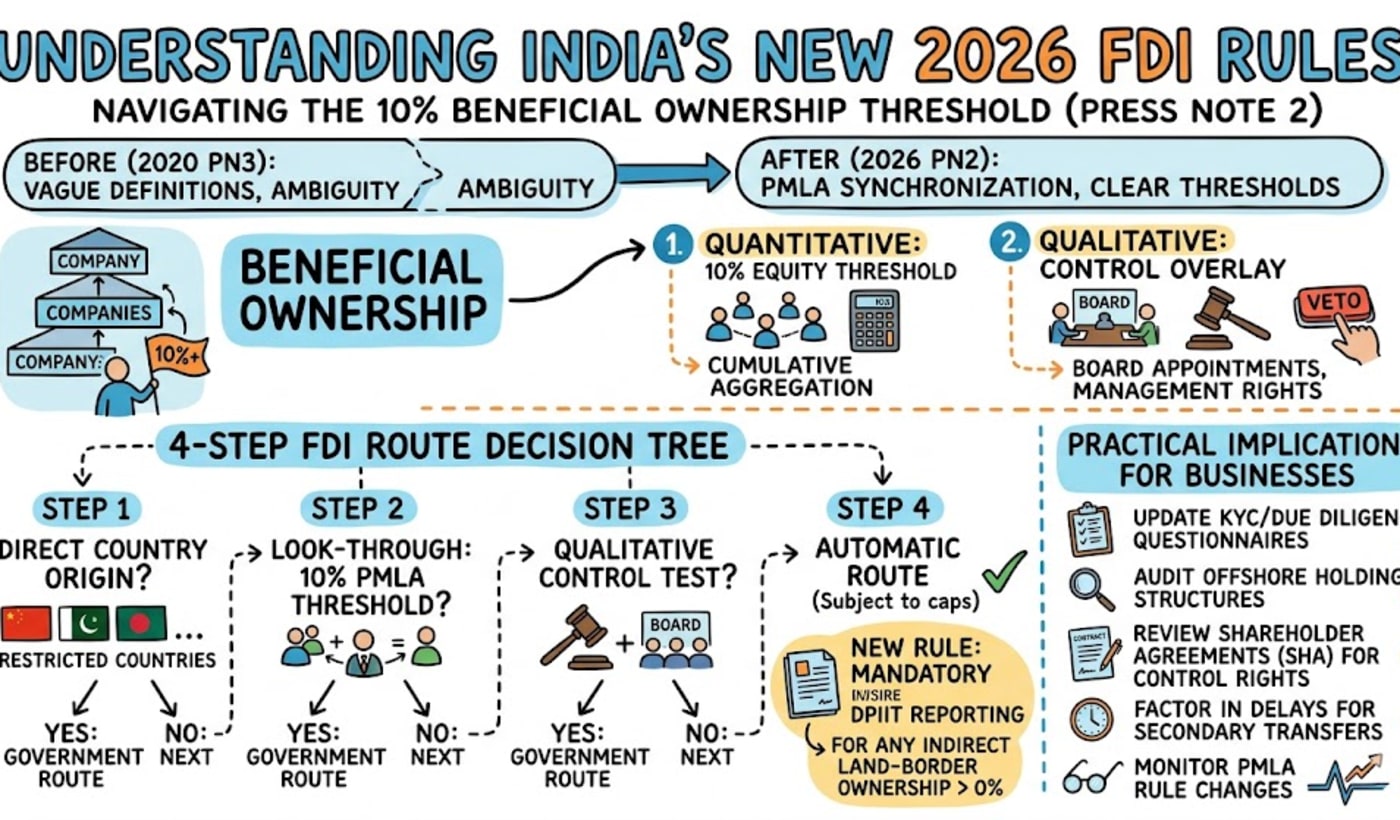

If your business structure involves foreign investment, the regulatory landscape has just experienced a major shift. With the release of Press Note 2 (2026 Series), the Government of India has introduced strict, mathematically precise rules for inbound Foreign Direct Investment (FDI) originating from countries that share a land border with India.

Here is what you need to know to keep your investment structures compliant.

The Big Picture: Why Did the Rules Change?

Back in April 2020, India restricted FDI from neighboring land-border countries (China, Pakistan, Bangladesh, Nepal, Bhutan, Myanmar, and Afghanistan), requiring mandatory Government approval for these investments. However, the 2020 rules were vague about "beneficial ownership" — leaving a loophole where restricted funds could be routed through intermediary countries like Singapore or the Netherlands.

The 2026 amendment permanently closes this gap. For the first time, India's FDI policy officially adopts the strict definitions used in the Prevention of Money-laundering Act (PMLA).

What Changed: 2020 vs. 2026

| Feature | The 2020 Rules | The 2026 Rules |

| Beneficial Ownership | Undefined and vague | Strictly defined using PMLA standards |

| Trigger Threshold | No specific equity percentage | 10% ownership triggers restrictions |

| Hidden Control | Assessed on general principles | Explicit checks for veto rights and board control |

| Secondary Transfers | Not clearly addressed | Prior Government approval now explicitly required |

| Sub-threshold Reporting | No reporting required | Mandatory reporting to DPIIT for any stake > 0% |

The 4-Step Investment Assessment Check

To figure out if an investment requires Government Route approval, you must evaluate the transaction through this specific sequential framework.

Action Plan for Businesses and Investors

This amendment has immediate consequences for private equity funds, joint ventures, and corporate restructurings. Take these steps immediately to ensure compliance:

-

Update your KYC: Investor questionnaires must now specifically ask for beneficial ownership data tracking up to the ultimate owner, keeping the 10% PMLA threshold in mind.

-

Audit holding structures: Review the ownership of any intermediary offshore companies (like those in Mauritius, Singapore, or the US) to aggregate and calculate any land-border exposure.

-

Check Shareholder Agreements (SHAs): Ensure minority investors from restricted countries do not hold "affirmative voting rights" or veto powers that could trigger the qualitative control test.

-

Prepare for secondary transfer delays: If a corporate restructuring or buyout pushes a restricted entity's indirect holding above the 10% mark, you must secure Government approval before completing the transfer.

Disclaimer: This overview is for informational purposes only and does not constitute legal advice. Always consult with legal counsel and your wealth management advisor before executing cross-border transactions.