Residential Status Under FEMA vs. Income Tax Act 2025: The Critical Differences Every NRI Must Know

For Non-Resident Indians (NRIs) and global investors, tracking time spent in India is a standard routine. However, a widespread and costly mistake is assuming that your residential status is identical across all Indian laws.

In reality, residential status under FEMA (Foreign Exchange Management Act) and the Income Tax Act, 2025 operate on completely different wavelengths.

An individual can easily be classified as a "Resident" under FEMA while remaining a "Non-Resident" for tax purposes—or vice versa. Misunderstanding this distinction can result in illegal bank account maintenance, unauthorized property acquisitions, and severe regulatory penalties.

At Wealthpath Group, we untangle these complex cross-border frameworks to keep your global investments fully compliant.

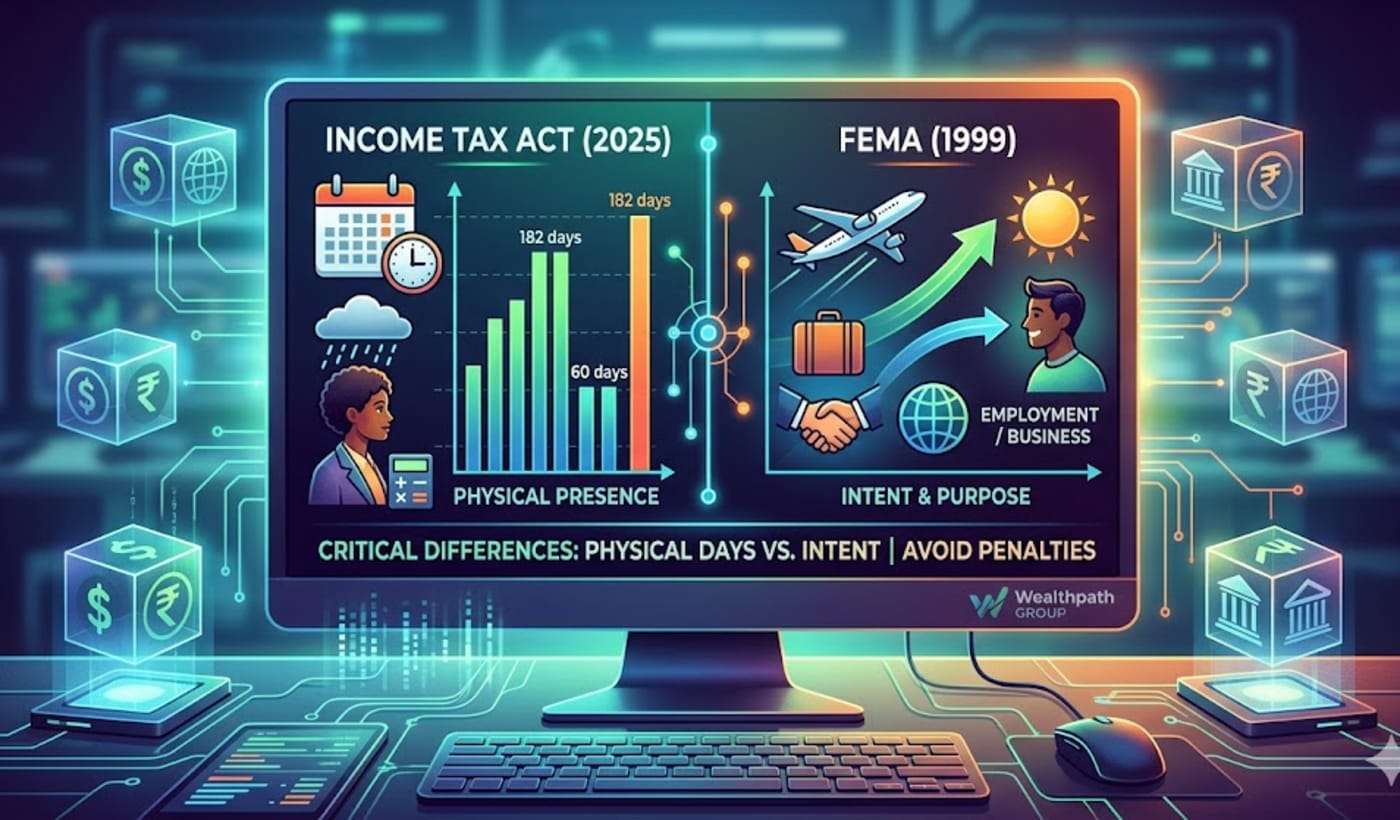

The Core Clash: Intent vs. Physical Presence

The fundamental conflict between exchange control laws (FEMA) and tax laws (Income Tax Act, 2025) comes down to why you are moving versus how long you have stayed.

1. Income Tax Act, 2025: A Strict Number Game

Under Section 6 of the Income Tax Act, 2025, tax residency is determined purely by mathematical calculation and physical presence within a specific tax year (running from April 1 to March 31).

Generally, you are a tax resident if:

-

You spend 182 days or more in India during the financial year.

-

Alternatively, you spend 60 days or more in the current financial year AND have been in India for 365 days or more across the preceding 4 years. (Note: For Indian citizens or PIOs visiting India with Indian-sourced income exceeding ₹15 Lakhs, this 60-day window is extended to 120 days).

Your intent, job offers, or long-term plans do not matter to the tax department; only the physical days stamped on your passport do.

2. FEMA 1999: Driven by Purpose and Intent

FEMA focuses on the economic center of your life and your financial intent. Under FEMA, physical stay is secondary to the purpose of your relocation.

You become a Person Resident Outside India (PROI/NRI) under FEMA the very moment you leave India for:

-

Taking up employment outside India.

-

Carrying on a business or vocation outside India.

-

Any other purpose indicating an intention to stay outside India for an uncertain period.

The Day-One Rule: If you move to Dubai or London on an employment visa on June 1st, you become a Non-Resident under FEMA on day one. You do not need to wait 182 days. Conversely, under the Income Tax Act, 2025, you might still remain a tax resident of India for that financial year because you spent April and May in the country.

Summary Comparison: FEMA vs. Income Tax Act 2025

| Feature | Income Tax Act, 2025 | FEMA, 1999 |

| Primary Objective | To determine the scope of taxable income in India. | To regulate foreign exchange inflows, outflows, and asset holdings. |

| Basic Criterion | Physical presence (counting exact days). | Purpose of stay and long-term intent. |

| Period of Evaluation | Evaluated strictly per financial year. | Evaluated dynamically based on changing circumstances or employment status. |

| The Intermediate Category | Features a temporary RNOR (Resident but Not Ordinarily Resident) status. | No intermediate status; you are either a Resident or a Non-Resident. |

| Impact of Violation | Interest, reassessment, and tax penalties. | Compounding fees or penalties up to 300% of the transaction value. |

Real-World Trap: The Returning NRI

Consider an NRI who moves back to Ahmedabad after a decade in the US to set up a consulting practice.

-

Tax Angle (Income Tax Act, 2025): Thanks to the RNOR (Resident but Not Ordinarily Resident) provision, this individual can enjoy tax-exempt status on their foreign-sourced income for up to 2 to 3 years after returning.

-

FEMA Angle: The moment this individual lands in India with the intention of staying indefinitely or setting up a business, they instantly become a Resident under FEMA.

The Risk: If this returning professional continues to operate their old NRE/NRO bank accounts or foreign bank accounts without redesignating them into Resident/RFC (Resident Foreign Currency) accounts, they are in direct violation of RBI guidelines and face major penalties.

Align Your Compliance with Wealthpath Group

Navigating the transition to the Income Tax Act, 2025 alongside evolving RBI notifications requires clear legal coordination. Miscalculating your status under either law can disrupt your investments, freeze bank accounts, or trigger tax audits.

At Wealthpath Group, we bridge this gap by providing synchronized advisory services:

-

Simultaneous evaluation of your legal status under both FEMA and Direct Tax frameworks.

-

Streamlined conversion and management of NRE, NRO, and RFC bank accounts.

-

End-to-end guidance on cross-border property transactions, inheritances, and corporate investments.

-

Comprehensive compliance tracking to match your physical calendar with your legal intent.

Don't let split regulatory definitions put your wealth at risk. Contact Wealthpath Group today to speak with our cross-border compliance experts and secure your financial roadmap.