Comprehensive Guide to Section 270A of the Income Tax Act: Penalties for Under-Reporting and Misreporting of Income

As tax compliance norms become increasingly stringent in India with enhanced scrutiny, real-time data matching, and faceless assessments, understanding the penal provisions of the Income Tax Act is no longer optional—it is a necessity. Introduced by the Finance Act of 2016 (applicable from FY 2016-17) as a replacement for the older Section 271(1)(c), Section 270A is the primary provision dealing with penalties for the under-reporting and misreporting of income.

Whether you are a salaried individual, a freelancer, or a business owner, failing to disclose your actual income or inflating your deductions can invite severe financial repercussions. In this comprehensive guide, we will break down the intricacies of Section 270A, the difference between under-reporting and misreporting, penalty calculations, and how you can claim immunity.

What is Section 270A of the Income Tax Act?

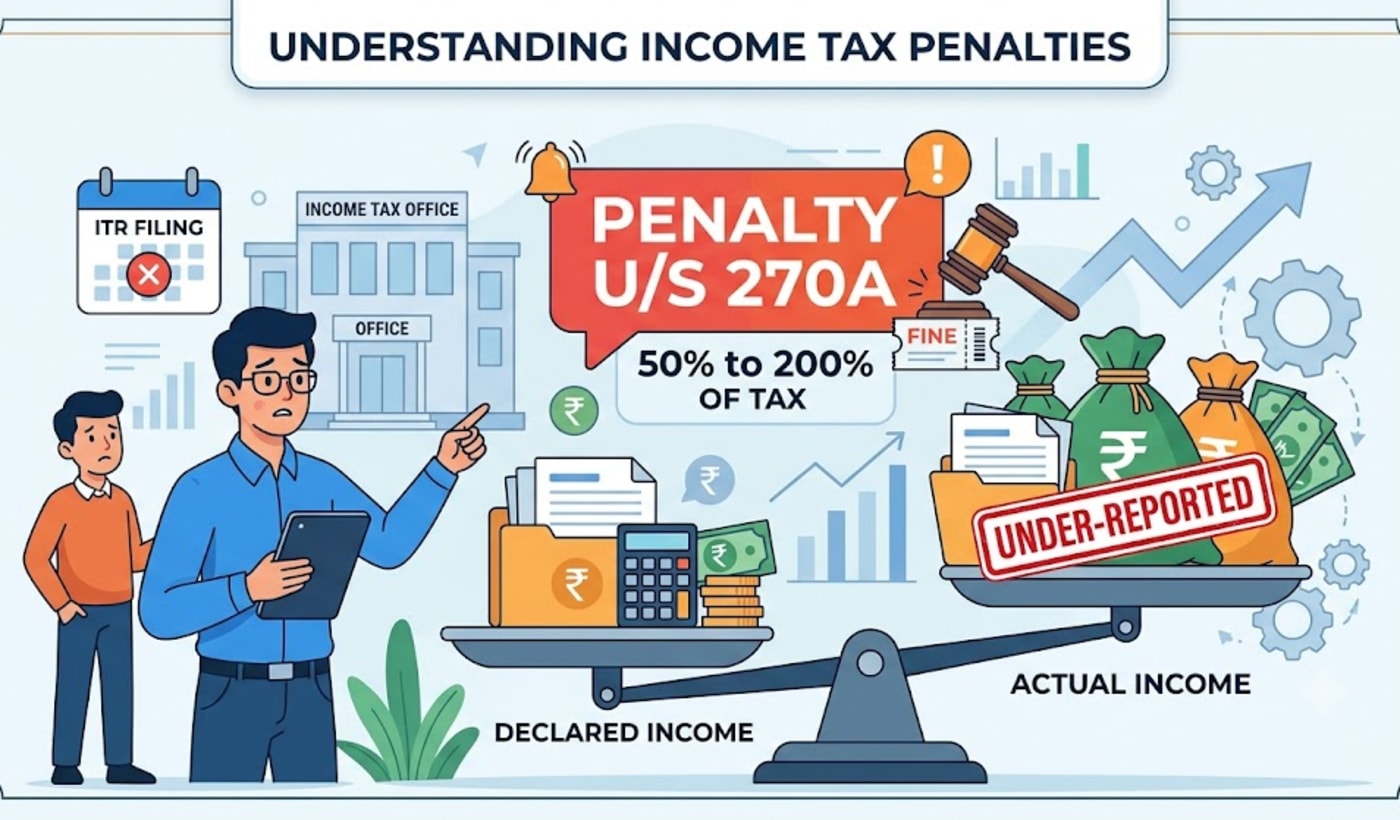

Section 270A empowers the Assessing Officer (AO), the Commissioner (Appeals), or the Principal Commissioner to levy a penalty on a taxpayer who has under-reported or misreported their income.

The core objective of this section is to penalize tax evasion, ensure accurate disclosure of financial transactions, and maintain the integrity of the tax system. Depending on the severity and intent behind the inaccurate filing, the penalty ranges from 50% to 200% of the tax payable on the undisclosed amount.

Under-Reporting vs. Misreporting of Income

To apply the penalty accurately, the Income Tax Act draws a strict line between "under-reporting" (which may sometimes stem from negligence) and "misreporting" (which involves deliberate deception).

1. Under-Reporting of Income (50% Penalty)

Under-reporting occurs when the income assessed by the tax department exceeds the income declared by the taxpayer in their Income Tax Return (ITR), or when a taxpayer fails to file a return altogether, and their assessed income exceeds the basic exemption limit.

Common causes of under-reporting include:

-

Failing to declare interest earned from savings accounts or Fixed Deposits (FDs).

-

Miscalculating freelance or business income.

-

Omitting capital gains from mutual funds, stocks, or real estate.

-

Unintentional bookkeeping errors or clerical mistakes.

Penalty Rate: For under-reporting, the penalty is 50% of the tax payable on the under-reported income.

2. Misreporting of Income (200% Penalty)

Misreporting is treated as a grave offense. Under Section 270A(9), under-reporting is classified as misreporting if it is a consequence of deliberate fraud, falsification, or suppression of facts.

Statutory examples of misreporting include:

-

Misrepresentation or suppression of material facts.

-

Failure to record investments in the books of account.

-

Claiming expenditure that is not substantiated by any evidence (e.g., bogus expenses/fake invoices).

-

Recording false entries in the books of account.

-

Failure to record receipts or international transactions.

Penalty Rate:

For misreporting, the penalty skyrockets to 200% of the tax payable on the misreported income.

Penalty Calculation under Section 270A (Example)

Let’s understand the financial impact of Section 270A through a practical example:

Scenario: Mr. Sharma, a consultant, declares a total taxable income of ₹10,00,000 for the financial year. During an assessment, the AO discovers that Mr. Sharma actually earned ₹15,00,000.

-

Under-reported / Misreported amount: ₹5,00,000.

-

Assuming a flat 30% tax bracket for simplicity, the tax payable on this ₹5,00,000 is ₹1,50,000.

Case A: Imposed for Under-Reporting

If the AO determines that the ₹5,00,000 was missed due to an honest oversight (e.g., forgetting to add a specific bank account's interest), it falls under "under-reporting".

-

Penalty: 50% of ₹1,50,000 = ₹75,000.

-

Total Liability: Tax of ₹1,50,000 + Penalty of ₹75,000 + Applicable Interest.

Case B: Imposed for Misreporting

If the AO discovers that Mr. Sharma intentionally created fake expense invoices worth ₹5,00,000 to suppress his profit, it constitutes "misreporting".

-

Penalty: 200% of ₹1,50,000 = ₹3,00,000.

-

Total Liability: Tax of ₹1,50,000 + Penalty of ₹3,00,000 + Applicable Interest.

When is the Penalty NOT Levied? (Exceptions under Section 270A)

The Income Tax Act is not entirely draconian. Section 270A(6) provides specific exclusions where an addition to income will not be treated as under-reported:

-

Bona Fide Explanations: The taxpayer offers an explanation for the discrepancy that the AO finds bona fide, and the taxpayer has disclosed all material facts.

-

Estimation Differences: The income was determined based on an estimate, but the accounts are correct and complete, and the accounting method makes exact calculation impossible.

-

Transfer Pricing Adjustments: Additions made by a Transfer Pricing Officer (TPO) where the taxpayer maintained proper documentation and acted in good faith.

-

Honest Interpretational Differences: If an addition is made simply because the tax department interpreted a complex tax law differently than the taxpayer, provided full disclosure was made in the ITR.

How to Claim Immunity from Penalty (Section 270AA)

To promote ease of doing business and reduce protracted tax litigation, the government introduced Section 270AA. This section allows taxpayers to apply for immunity from the imposition of the penalty under Section 270A and from prosecution proceedings under Section 276C/276CC.

Conditions to claim immunity:

-

The taxpayer must pay the assessed tax and interest within the period specified in the demand notice.

-

The taxpayer must not file an appeal against the assessment order.

-

The application for immunity must be made to the Assessing Officer within one month from the end of the month in which the assessment order was received.

-

Crucial Condition: Immunity under Section 270AA is only available for under-reporting. It cannot be granted if the penalty is initiated for misreporting of income.

(Note: Furthermore, under Section 273A, the Principal Commissioner or Commissioner holds discretionary powers to reduce or waive penalties in genuine cases, provided the taxpayer has made full and true disclosure voluntarily and cooperated during the inquiry).

Best Practices to Avoid Penalties Under Section 270A

With the CBDT utilizing AI, the Annual Information Statement (AIS), and the Taxpayer Information Summary (TIS), hiding income is nearly impossible. To stay compliant:

-

Reconcile Data: Always match your income with Form 26AS, AIS, and TIS before filing your return.

-

Report All Sources: Do not ignore minor income sources like savings bank interest, small capital gains, or foreign dividends.

-

Maintain Documentation: Keep legitimate bills, invoices, and receipts for all business expenses claimed.

-

File Updated Returns: If you discover a mistake after filing, use the provisions for Revised Returns (Sec 139(5)) or Updated Returns (Sec 139(8A)) to proactively pay your dues before the department sends a scrutiny notice.

Disclaimer: This article is strictly for informational purposes and serves as an audit compliance guideline. It does not constitute formal legal or tax advice. For specific tax-related queries, please consult a qualified Chartered Accountant or tax professional.